UPDATED 4/21/23

Have you tuned into news outlets lately? “The market is crashing!” or “we’re in a recession.” Wait, wait, wait… I don’t think so! You need to think local and focus on the local data, financial differences, and circumstances of our current real estate market in 2023, and listen to area experts, not spectators. This is what is happening in Connecticut:

– Limited inventory/supply

– High demand that increases daily

– Homes aren’t being built quickly enough to meet demands

– Millennial buyers continue to enter the real estate market in droves

– Remote work continues to enable buyers to live in a variety of areas

– Government programs – while rates have increased due to the Fed, the government has enabled home buying programs and increasing loan limits

There is a “tale between two coasts,” so, what’s going on here in Connecticut, especially in Fairfield County? We felt a slight dip in values in December of 2022, followed by a surge at the end of January, sending home values and offers up anywhere between 2-10%+ over their asking price. Two of our listings in April had over 50 showings and 11 and 26 offers respectively. This shows that our inventory is still incredibly low and our buyer pool is growing on a daily basis.

So is our housing market crashing? No, it is not. Might we see a stabilization in the near future? Potentially, but we are still seeing a strong market for sellers when a home’s price reflects its current condition. So, how long do you plan to sit on the sidelines before taking advantage of the tremendous equity in your home?

Will this bubble burst?

If you’re waiting for the housing bubble to burst, you might have to wait a little bit longer in Connecticut. As rates decline, more buyers will enter the already limited housing market and I expect we will continue to see bidding wars, strong offers, and limited (unless you’re lucky and a home was overpriced to start!) negotiations. The local data and actions speaks for itself.

PUBLISHED 2/24/23

Limited Housing Inventory

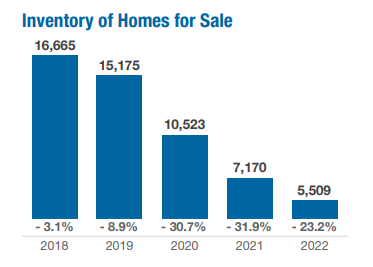

While our home values are stabilizing, our inventory is still incredibly low. Q3 and Q4 in 2022 showed a slightly slower market due to the rate increases but as buyers adjusted, some mortgage companies got creative, and January 2023 took off! When homes are priced well, we are still seeing multiple bids.

The first chart below from SmartMLS demonstrates the housing supply (inventory) for the past 5 years in Connecticut. The second chart from Raveis.com demonstrates the housing supply for the past 12 months in Connecticut. Inventory is incredibly low, and we have limited supply and that is driving up market value.

So is our housing market crashing? No, it is not. Might we see a stabilization in the near future? Potentially, but we are still seeing a strong market for sellers when a home’s price reflects its current condition. That is and always will be key.

Mortgage Standards

In the early 2000’s there were more lenient guidelines for mortgage approval, which created a false sense of buying power for homeowners and risk for lending companies. As a result, homeowners were defaulting on their loans in 2008 and thereafter, and we saw an uptick foreclosures and reductions in home values which then led to short sales. Today, we have strict lending guidelines, ensuring that buyers are well-qualified for the specific homes they are buying.

Wins for Our Clients and What We Are Experiencing

In mid-February, there was a home listed for sale in Fairfield, for lower than it should have been listed for ($514,000—I would have priced it at $599,000 due to the neighborhood and potential). That house had 84 showings, 24 offers, and went over $650,000. That is not a crash, that’s an explosion.

On the flipside, there was an older home listed for $499,000 in Trumbull that has been on the market for 130 days. I was able to secure a fabulous purchase price for my client of $459,500, along with getting inspection items taken care of. Had that homeowner priced their house slightly lower (at market value vs above market value) they would have had multiple bids and it would have sold faster and likely for more than what my buyer is purchasing it for. Of course, I’m glad they didn’t, it was a win for my homebuyer!

If you’re buying or selling in the luxury market, that is still a gloriously strong market in our area as well. In previous years, the luxury home would be listed for sale for 6+ months to even a few years, but that is not the case anymore. A home in Southport that was listed for $5.9M sold for $6.2M, and for the luxury market, if a home sells under the asking price, the sale price is within 95% of the asking price.

Let’s look at the data:

The median sale price in ALL of Fairfield County in February of 2022 for single family homes was $570,000 and today, the median sale price in Fairfield County of homes that are currently pending sale is $689,000.

The average days on market is currently 68 days and in February of 2022 it was 61. I do think days on market has increased due to buyers “testing” the market at a premium price vs fair market value. The result is a home that stays on the market longer.

Our Advice to Buyers and Sellers

Are there deals to be had? Yes, if you know where to look and how to negotiate, absolutely, but there are also phenomenal seller opportunities as well. My advice to both buyers and sellers is to continue to put your best foot forward.

Sellers, price your home at market value and let buyers drive up your value. I understand wanting to ask a premium to see what offers you might receive but in today’s market that is counterproductive, you will regret that decision in the end. If a home does not sell within a week or two, in this market, buyers question why, and you will be leaving money on the table. If you price at a competitive, market value, you might end up with more than you had even hoped for!

Buyers, continue to save, continue to be aggressive with your offers, and have an agent that will be honest with you about a true value and will advocate for you and most importantly, prospect for off-market homes for you. If you feel that you are “overpaying” slightly, it’s okay. You’ve purchased your dream home, you’re paying yourself, you’re building up equity and that is more than you would be doing if you were renting.

Get Creative to Lock in a Lower Rate so You Can Move!

If you haven’t heard of a 2-1 buydown, we suggest you reach out to your lender to learn about a temporary buy-down option that puts you in a comfortable mortgage rate. There are many sellers that are locked in to a fabulous 2-3% interest rate that need to move but are hesitant to make a move due to the current rate (which is in the 5-6%’s). If you take advantage of a 2-1 buy down, you can buy your rate down, up to 2%. A 5% rate could become 3% (-2%) for the first year, and a 5% rate becomes a 4% rate (-1%) for the second year. You can get the home of your dreams and a great rate.

The Bottom of the Bubble, the Bottom Line!

Home prices may ebb and flow slightly, but you will not see a crash here in Connecticut like we saw in 2008. If this is a concern you have, we’re happy to meet with you to discuss your current home’s value, your next steps, and how you can take advantage of the financial position this puts you in!